Home

/ How To Find Average Cost In Economics - Fixed costs are the costs that are independent of the number of goods produced, or the costs incurred when no goods are produced.

How To Find Average Cost In Economics - Fixed costs are the costs that are independent of the number of goods produced, or the costs incurred when no goods are produced.

How To Find Average Cost In Economics - Fixed costs are the costs that are independent of the number of goods produced, or the costs incurred when no goods are produced.. Total variable cost is the opposite of fixed costs. So our fixed cost is $50. The result is 50 + 6 x 0 = 50. So using the two given equations for total cost, take the first derivate of total cost to find the expressions for marginal cost: How do you calculate average fixed cost?

That means the total cost goes up by 6 whenever an additional good is added, as shown by the coefficient in front of the q. The total cost would be $250 + $140 = $390. The most accurate way of calculating the marginal cost is with calculus. This video explains how to find the average cost function and find the minimum average cost given the total cost function.site: Tc total costs = fc+vc.

Microeconomics Cost Functions from image.slidesharecdn.com That means the total cost goes up by 6 whenever an additional good is added, as shown by the coefficient in front of the q. Let's say you want to calculate marginal cost, total cost, fixed cost, total variable cost, average total cost, average fixed cost, and average variable costwhen given a linear equation regarding total cost and quantity. A chart will typically provide information regarding the cost of producing one good, the marginal cost ,and fixed costs. Suppose it's producing two goods, and company officials would like to know how much costs would increase if production was increased to three goods. (1) find total quantity, (2) calculate total cost, and (3) divide total cost by total quantity. So using the two given equations for total cost, take the first derivate of total cost to find the expressions for marginal cost: You can learn the variable cost of production by again referencing the profit. These are the costs that change when more is produced.

Total variable cost is the opposite of fixed costs.

That means the total cost goes up by 6 whenever an additional good is added, as shown by the coefficient in front of the q. Tc total costs = fc+vc. See full list on thoughtco.com See full list on thoughtco.com Let's say you want to calculate marginal cost, total cost, fixed cost, total variable cost, average total cost, average fixed cost, and average variable costwhen given a linear equation regarding total cost and quantity. Let's say the cost of producing one good is $250, and the marginal cost of producing another good is $140. For example, if it costs $600 to produce three goods and $390 to produce two goods, the difference is 210, so that's the marginal cost. How do you find total variable cost in economics? For instance, the total variable cost of producing four units is calculated thus: Fixed cost is found when q = 0. How do you find the average cost function? Marginal costis the cost a company incurs when producing one more good. So our fixed cost is $50.

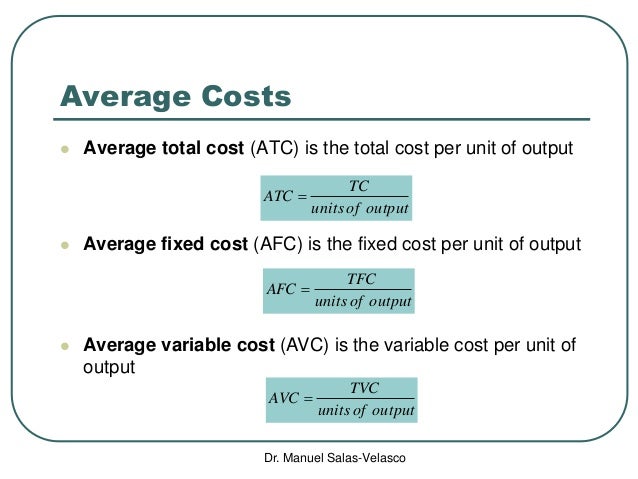

Average total cost (atc) is calculated by dividing total cost by the total quantity produced. Determine the fixed cost of production. Marginal costis the cost a company incurs when producing one more good. For example, if it costs $600 to produce three goods and $390 to produce two goods, the difference is 210, so that's the marginal cost. See full list on thoughtco.com

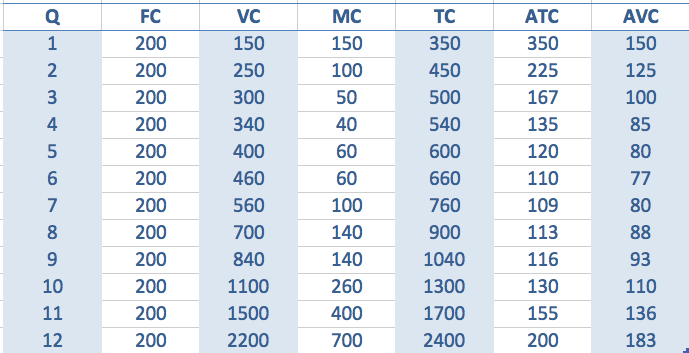

Average Cost Economics Help from www.economicshelp.org Sometimes a table or chart will give you the marginal cost, and you'll need to figure the total cost. To find the fixed cost of production, start by looking at a business's profit. See full list on thoughtco.com You can figure the total cost of producing two goods by using the equation: How do you find total variable cost in economics? Tc total costs = fc+vc. Let's say the cost of producing one good is $250, and the marginal cost of producing another good is $140. Total variable cost is the opposite of fixed costs.

Remember that fixed cost is the cost we incur when no units are produced.

Average total cost (atc) is calculated by dividing total cost by the total quantity produced. These are the costs that change when more is produced. The result is 50 + 6 x 0 = 50. See full list on thoughtco.com The total cost would be $250 + $140 = $390. Total cost is represented by tc. The difference is the marginal cost of going from two to three. Let's say the cost of producing one good is $250, and the marginal cost of producing another good is $140. Nonlinear total cost equations are total cost equations that tend to be more complicated than the linear case, particularly in the case of marginal cost where calculus is used in the analysis. Average variable cost (avc) is calculated by dividing variable cost by the quantity produced. To find the fixed cost of production, start by looking at a business's profit. For instance, the total variable cost of producing four units is calculated thus: You will learn about the price system, which helps to coordinate global economic activity.

Nonlinear total cost equations are total cost equations that tend to be more complicated than the linear case, particularly in the case of marginal cost where calculus is used in the analysis. This means there is a constant marginal cost of $6 per unit produced. Average total cost (atc) is calculated by dividing total cost by the total quantity produced. To find the fixed cost of production, start by looking at a business's profit. So to find the fixed cost, substitute in q = 0 to the equation.

Average Cost Types Classifications Averge Fixed Cost Afc Average Vaiable Cost Avc Average Total Cost Atc Definition And Explanation Formula Example Diagram Curve Economicsconcepts Com from www.economicsconcepts.com This video explains how to find the average cost function and find the minimum average cost given the total cost function.site: In this case, let's say it costs $840 to produce four units and $130 to produce none. For total cost, the formulas are given. Average cost or average total cost average cost (ac), also known as average total cost (atc), is the average cost per unitof output. To find the fixed cost of production, start by looking at a business's profit. See full list on thoughtco.com Let's say you want to calculate marginal cost, total cost, fixed cost, total variable cost, average total cost, average fixed cost, and average variable costwhen given a linear equation regarding total cost and quantity. So the total cost of producing 10 units is 50 + 6 x 10 = 110.

(1) find total quantity, (2) calculate total cost, and (3) divide total cost by total quantity.

You will learn about the price system, which helps to coordinate global economic activity. Marginal cost is essentially the rate of change of total cost, so it is the first derivative of total cost. Feb 22, 2021 · how to calculate average cost 1. Marginal costis the cost a company incurs when producing one more good. How do you calculate average fixed cost? Find the variable cost of production. Fixed costs are the costs that are independent of the number of goods produced, or the costs incurred when no goods are produced. (1) find total quantity, (2) calculate total cost, and (3) divide total cost by total quantity. For total cost, the formulas are given. Average cost (ac) is the total cost (tc) divided by quantity. You will learn about the price system, which helps to coordinate global economic activity. Total cost is simply all the costs incurred in producing a certain number of goods. See full list on economicshelp.org

For this exercise, let's consider the following two equations: how to find average cost. You will learn about the price system, which helps to coordinate global economic activity.